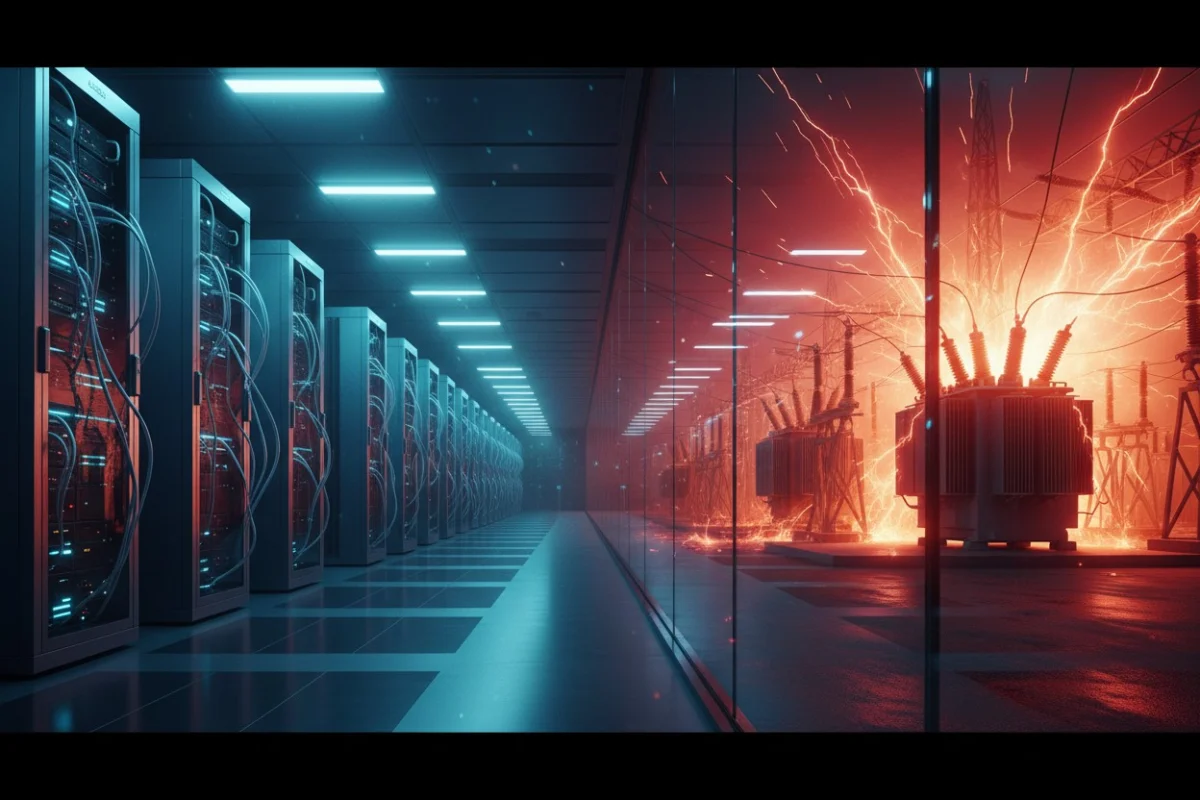

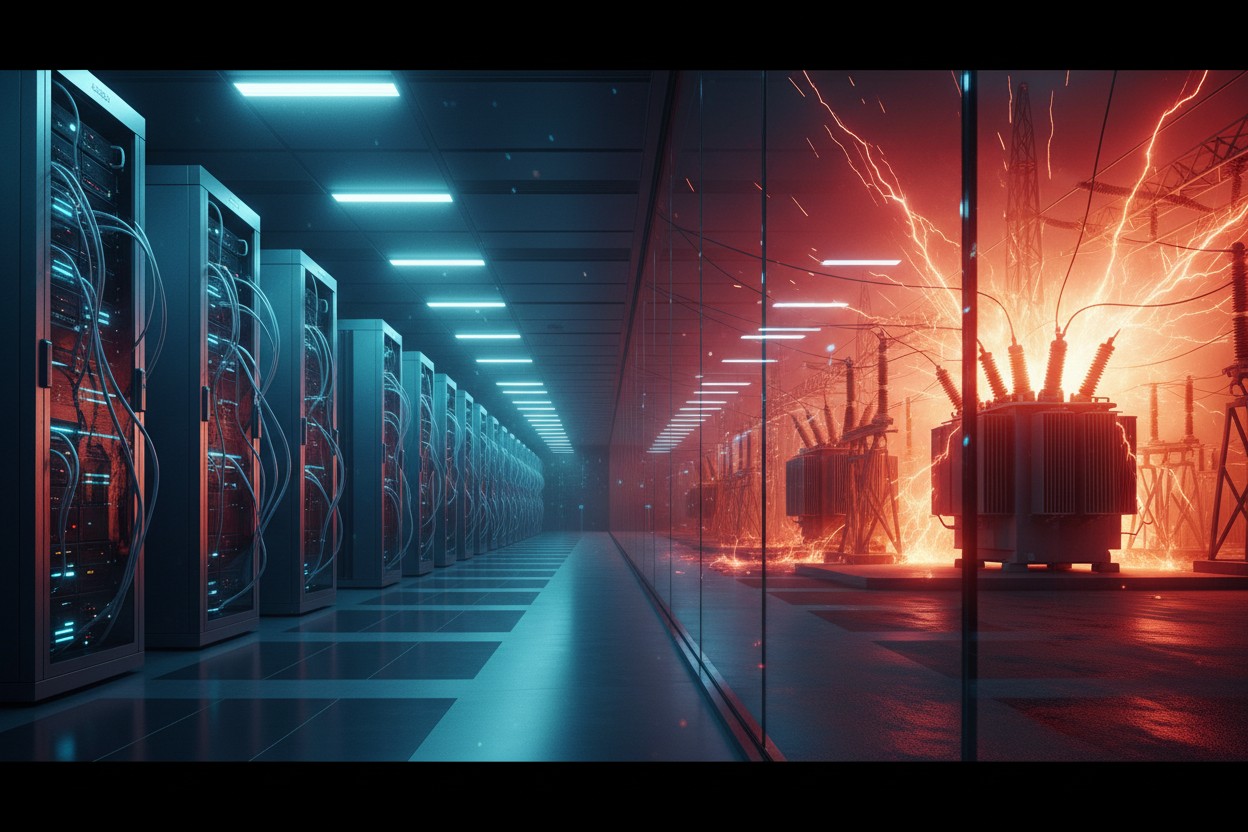

The rapid ascent of artificial intelligence is no longer merely a story of computational breakthroughs and algorithmic sophistication. It has evolved into a high-stakes industrial drama centered on a singular, finite resource: electricity. As tech giants and sovereign nations race to build the massive data centers required to train and host the next generation of Large Language Models (LLMs), they have collided with a hard, physical ceiling—the aging and capacity-strained electrical grids of the modern world.

Industry projections are staggering. According to estimates cited by McKinsey and JLL, global infrastructure spending linked to AI could balloon to over $5 trillion by 2030. Yet, the physical reality is sobering: data centers currently consuming roughly 60 gigawatts (GW) of power are expected to see that demand surge toward 300 GW by the end of the decade. This trajectory represents a 20 percent annual rise in electricity consumption—a growth rate unseen since the dawn of the Industrial Revolution.

The Grid Under Siege: A Chronology of the Crisis

The crisis did not emerge overnight, but it has reached a breaking point in the 2025–2026 period.

- 2023–2024 (The Awareness Phase): Major grid operators in North America began documenting unprecedented interconnection request queues. Developers of AI campuses, each demanding hundreds of megawatts, began submitting applications that would effectively double the load of entire municipal utility districts.

- 2025 (The Infrastructure Crunch): A profound shortage of large power transformers became the primary bottleneck. As Wood Mackenzie reported, U.S. spending on power generation equipment for data centers surged to $20 billion, yet supply chains remained unable to keep pace with demand.

- 2026 (The Reality Check): The year has been defined by project cancellations. As noted by investors like Kevin O’Leary, roughly half of all data centers scheduled for 2026 completion are facing indefinite delays or outright cancellation due to the simple lack of available grid capacity.

- 2027–2030 (The Strategic Pivot): We are currently entering a phase where the "hyperscalers"—Amazon, Microsoft, Google, and Meta—are pivoting away from public grid reliance toward "behind-the-meter" power generation, including nuclear, hydro, and massive battery storage systems.

Supporting Data: The Scale of the Disruption

The figures regarding the sheer scale of the power requirement are, by any measure, gargantuan. The National Electrical Manufacturers Association (NEMA) projects that data center electricity consumption in the United States will rise by 300 percent over the next decade. By 2037, these facilities are expected to account for a staggering 38 percent of total net electricity consumption in the U.S.

To put this in perspective, a single modern AI campus can require the same amount of power as a mid-sized city. The existing infrastructure, designed for a world of decentralized residential and light-industrial consumption, is struggling to adapt to these massive, concentrated point-loads. Furthermore, the cost of equipment is soaring; the $20 billion spent on data center power equipment in 2025 is projected to triple to $65 billion by 2030, a direct consequence of both inflation and the scarcity of specialized electrical hardware.

Official Responses and Regulatory Alarm

The gravity of the situation has reached the halls of Congress. Seven major U.S. grid operators recently issued a joint warning to federal legislators, characterizing the rapid load growth from AI as a direct threat to national grid reliability. The consensus among these operators is clear: economic growth and the push for total electrification are outpacing infrastructure development by a dangerous margin.

The regulatory environment in the United States is further complicated by the "interconnection queue" process. Utilities report multi-year wait times for studies that determine whether a grid can handle a new load. For a sector that operates on a 12-to-18-month hardware deployment cycle, a five-year wait for a grid connection is essentially a death sentence for a project.

Nvidia CEO Jensen Huang has been vocal about the geopolitical implications of this grid bottleneck. Huang has cautioned that the United States risks falling behind in the AI arms race, not because of a lack of silicon, but because of energy policy. He points to nations like China, where state-subsidized energy costs and streamlined, centralized regulatory frameworks allow for the rapid deployment of power-intensive infrastructure that would take years to permit and build in Western markets.

Tech Giants: The Shift to Sovereign Power

Facing a grid they can no longer rely on, Big Tech is acting as its own utility. Amazon Web Services (AWS) has initiated extensive dialogues with nuclear power providers, aiming to secure long-term power purchase agreements (PPAs) that bypass the public grid entirely. It is estimated that utilities owning roughly one-third of all U.S. nuclear capacity are currently in active discussions with data center operators.

This shift is not limited to the U.S. In Kenya, a $1 billion joint venture between Microsoft and G42—intended to be a landmark for African AI infrastructure—has effectively stalled due to irreconcilable disagreements over power capacity. These failures demonstrate that the ability to secure energy is now the primary determinant of a company’s ability to compete in the AI ecosystem.

Case Study: The Bitzero Model

Amidst this chaos, companies that secured power before the frenzy began have gained a distinct competitive advantage. Bitzero (NASDAQ: AIBZ) serves as a prime example of the "energy-first" strategy. By securing low-cost hydroelectric power in Norway and Finland, the company has insulated itself from the volatility and shortages plaguing the rest of the market.

Bitzero currently controls a development pipeline exceeding one gigawatt, with its 110 MW campus in Namsskogan, Norway, serving as a blueprint for the future. With direct access to the 132-kilovolt transmission network and an all-in electricity cost of three to four cents per kilowatt-hour, the company is able to operate profitably while others struggle to even procure power. In May 2026, the company cemented its position by signing a 15-year, $2.6 billion lease with OneQode Networks. This deal underscores a broader trend: in a world of power scarcity, control over the source of energy is more valuable than control over the server hardware itself.

Implications: The New Strategic Reality

The implications for the next decade are profound. Investors who once focused exclusively on semiconductor design and model architecture are now forced to become energy analysts. The "AI Factory" of the future will not be located where talent is cheapest, but where energy is most abundant and accessible.

1. The Death of the "Build Anywhere" Model

The era of siting data centers near talent hubs or tax-incentive zones is closing. New data center developments will be tethered to power generation assets—be it wind farms, hydroelectric dams, or Small Modular Reactors (SMRs).

2. The Rise of "Smart" Grids

As William Scott explores in AI Everyday, the only way to manage this load will be through the integration of AI-driven smart grids. Algorithms that can analyze supply and demand in real-time will be necessary to prevent total system collapse. However, as currently stands, the demand outpaces these management tools.

3. Geopolitical Power Shifts

Nations with legacy energy infrastructure that is either too expensive or too fragile will lose their seat at the AI table. Conversely, nations with large-scale, low-cost, renewable energy profiles (such as those in Scandinavia or parts of Canada) will become the new "Silicon Valleys" of the world, serving as the physical bedrock for the global AI economy.

4. The Valuation of Utility

Expect to see a massive valuation adjustment in the utility sector. Companies that own large-scale power generation and have the rights to expand transmission will likely become the most sought-after M&A targets by major tech firms.

Conclusion

The bottleneck is not silicon; it is electrons. While the media focus remains on the latest GPU release from Nvidia or the newest model launch from OpenAI, the true constraint on the future of intelligence is the hum of the power transformer and the capacity of the high-voltage transmission line.

As Kevin O’Leary succinctly put it, the announced data centers that do not have ironclad power contracts are effectively "ghost projects." We are witnessing a fundamental shift in the global economy where energy independence is the prerequisite for technological sovereignty. In the coming years, the winners of the AI race will not be those with the fastest processors, but those who successfully secured the power to run them. The "Great Energy Bottleneck" is the defining challenge of the decade, and it is reshaping the industrial landscape from the ground up.