The biotechnology sector has entered a period of robust resurgence, marking the first half of 2026 as one of the most prolific periods for venture capital investment in recent memory. Despite a complex geopolitical landscape, shifting regulatory tides at the Food and Drug Administration (FDA), and a narrowing focus on early-stage innovation, the industry has demonstrated remarkable resilience. According to data tracked by BioPharma Dive, the life sciences venture landscape is currently defined by high-value "megarounds," a thriving merger and acquisition (M&A) environment, and a cautious but deep-pocketed investor base that is recalibrating what it means to back a "winning" drug startup.

Main Facts: A Half-Year of Massive Capital Influx

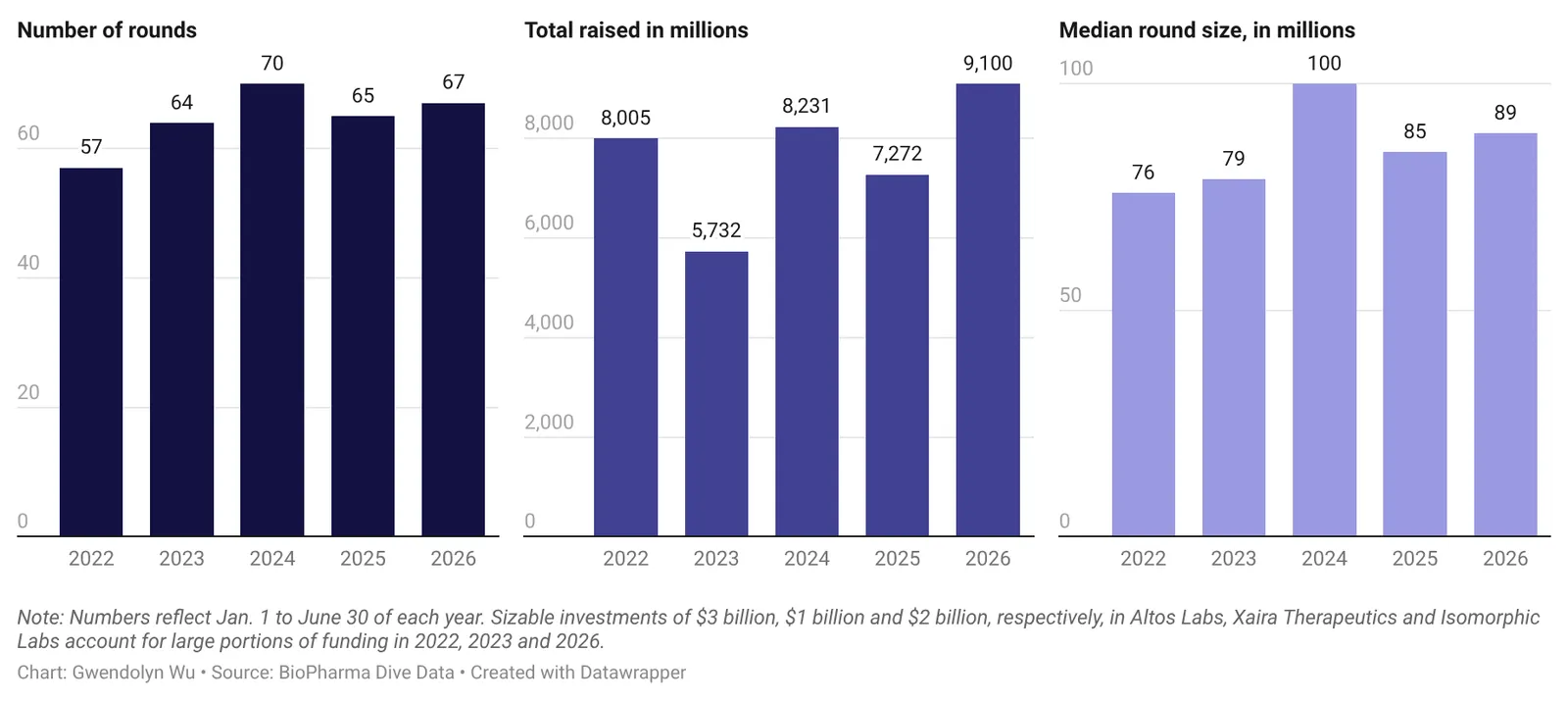

Between January and June 2026, the biotechnology venture ecosystem witnessed a significant influx of liquidity. At least 68 prominent biotech firms secured a combined total of more than $9.1 billion in venture funding. This figure represents the highest first-half total since the start of 2022, signaling a definitive recovery from the post-pandemic cooldown that had previously dampened market enthusiasm.

The primary characteristic of this funding surge is the concentration of capital. Approximately 76% of all funds raised during this period were funneled into "megarounds"—financing events worth $100 million or more. This indicates that while capital is abundant, it is being directed toward companies that have already reached a level of operational maturity, rather than being spread thinly across the broader, nascent startup landscape.

Chronology of the 2026 Biotech Market

To understand the current momentum, one must look at the specific catalysts that have defined the first six months of the year:

- Q1 2026: The year began with a renewed appetite for public offerings. As market volatility eased, biotech firms began testing the waters with IPOs, buoyed by positive data readouts from late-stage trials.

- April-May 2026: M&A activity accelerated rapidly. Major pharmaceutical players, seeking to replenish their pipelines to combat looming patent cliffs, turned to the private sector to acquire de-risked assets.

- June 2026: The close of the second quarter confirmed the "megaround" trend, underscored by the massive $2.1 billion infusion into Isomorphic Labs. This single event highlighted the growing intersection of artificial intelligence and drug discovery as a primary engine for venture interest.

Supporting Data: The Anatomy of Investment

The current investment climate is not monolithic; it reflects a deep-seated discernment among venture capitalists. The data reveals several key trends that define where the money is going and, perhaps more importantly, where it is not.

The "Safe Bet" Strategy

Investors are clearly prioritizing risk mitigation. Approximately two-thirds of all venture rounds (42 out of 68) were awarded to companies that already possessed at least one drug candidate in human clinical trials. This move away from "pre-clinical" speculation toward "clinical-stage" confidence is a direct response to the economic tightening that characterized the 2023–2024 period.

Sector-Specific Disparities

The capital allocation shows a distinct hierarchy of interest:

- Oncology and Immunology: These remain the "blue-chip" segments of biotech. More than 40% of all funding rounds in the first half of 2026 were dedicated to firms focused on cancer and immune-mediated diseases.

- Small Molecules and Biologics: Both modalities individually secured more than $2 billion in funding, proving that established, predictable drug-making platforms remain the industry’s backbone.

- Cell and Gene Therapy Slump: In contrast, the cell and gene therapy sector continues to struggle. These high-cost, high-risk platforms are on track to raise only about $2 billion for the entire year, a plateau that has persisted since 2022. Factors such as the disappointing commercial performance of therapies like Casgevy, coupled with clinical trial side-effect profiles, have cooled investor enthusiasm for this once-buzzy space.

Official Responses and Expert Analysis

Industry leaders and analysts suggest that the current environment is a "new normal"—one that rewards efficiency and proven platforms over speculative "moonshots."

Ben Zercher, a senior analyst at Pitchbook, notes that the sector is holding steady despite external pressures. "Venture capital has continued to go strong despite the threat of a U.S. government crackdown on investments in Chinese drug assets and turmoil at the FDA," Zercher remarked. He points to the "perfect storm" of regulatory instability as a reason for the current, more conservative investment posture.

Simeon George, CEO and managing partner of SR One, offers a broader philosophical perspective on the market. "The last few months have been reaffirming in terms of M&A," George noted in a recent interview. He acknowledges the nuance of the current market, adding, "The markets are a voting booth in the short term, and in the long term, they’re weighing scales."

Doreen Levine, a partner at Ernst & Young, echoes this sentiment regarding liquidity. "The VCs have the liquidity and interest to do it, it’s just that they’re being very judicious," she explained.

Implications for the Future of Innovation

While the $9.1 billion figure is undeniably positive, it masks a brewing crisis in the foundational layers of the industry. Ashwin Singhania, a principal at EY’s life sciences practice, warns that the decline in seed-round funding and the diminishing interest in first-time founders could have long-term consequences.

The Innovation Gap

"I think that a grave concern to the biotech community is where that next wave of early innovation is going to come from," Singhania stated. With the current preference for late-stage assets, the "seed" pipeline—the essential early-stage research that takes a concept from the bench to the bedside—is drying up. Compounding this issue are recent cuts to basic research funding at the National Institutes of Health (NIH), which many experts fear will create an "innovation vacuum" that could be felt as far as a decade from now.

The Geopolitical and Regulatory Backdrop

The industry is also navigating a shifting geopolitical landscape. The rise of companies like cAMPfield Therapeutics and Solstice Oncology, which often utilize ready-made assets from China, has invited intense scrutiny regarding national security and market competition. While these companies are successfully raising capital, they operate within a regulatory framework that is increasingly wary of international reliance for critical drug development.

The IPO and M&A Outlook

The 2026 market has seen 13 firms raise a combined $4.5 billion in IPO proceeds, with a median haul of $302 million—significantly higher than in years past. The fact that most of these debutants are trading above their initial price is a testament to the quality of the assets reaching the public market. Furthermore, with 38 acquisitions already logged this year, the M&A pace is the fastest it has been in seven years. This provides a crucial exit path for VCs, ensuring that the "liquidity flywheel" continues to turn.

Conclusion: A Cautious Expansion

The biotech industry in 2026 is defined by a paradoxical mix of extreme wealth and restricted access. While record-breaking amounts of capital are moving into the sector, they are being funneled through a narrow aperture of "safe" bets—late-stage clinical assets and established therapeutic modalities.

As the industry moves into the second half of the year, the primary challenge will be balancing this successful, risk-averse investment strategy with the need to cultivate the next generation of early-stage discovery. If the current trends continue, the sector will likely remain highly profitable and attractive to institutional investors, but stakeholders must remain vigilant that the desire for immediate, de-risked returns does not come at the expense of the basic research that sustains the future of medicine. The "weighing scales" of the market are currently tipped toward stability, but the long-term health of the industry may depend on how well it can bridge the gap between today’s massive megarounds and tomorrow’s foundational breakthroughs.