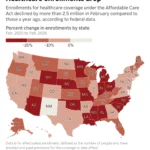

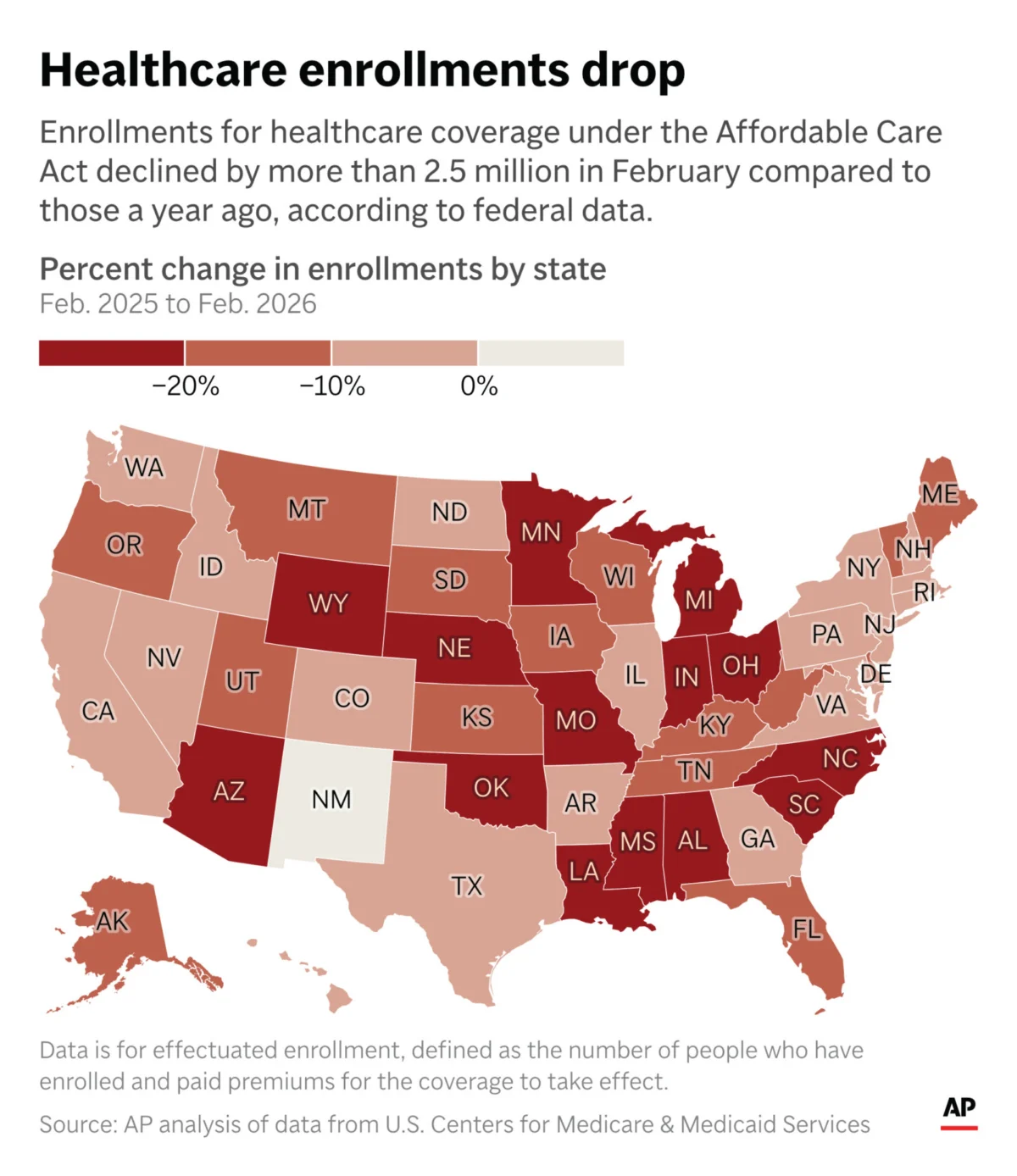

NEW YORK — The landscape of American healthcare is undergoing a seismic shift. Newly released federal data provides the first comprehensive, 50-state breakdown of a dramatic retreat from the Affordable Care Act (ACA) marketplace, revealing that approximately 2.6 million fewer Americans were enrolled in subsidized health insurance plans this February compared to the same period last year.

This sharp contraction—the first of its magnitude since the inception of the ACA—follows the January expiration of "enhanced" federal premium tax credits. As monthly insurance premiums for millions of families doubled or even tripled overnight, the resulting surge in costs has forced a significant segment of the population to weigh the necessity of healthcare against the reality of household budgets.

The Chronology of a Policy Pivot

The current crisis traces its origins to the legislative battles of late 2025. During the COVID-19 pandemic, federal lawmakers introduced enhanced premium subsidies designed to lower the out-of-pocket costs for marketplace insurance, effectively decoupling premiums from income ceilings for many. These credits fueled a record-breaking surge in enrollment, bringing millions of uninsured Americans into the system.

However, as the expiration date for these subsidies approached, a bitter partisan divide emerged in Congress. While Democrats and some moderate Republicans pushed for an extension of the financial support, the consensus failed to hold. When the subsidies expired on January 1, 2026, the marketplace was immediately transformed.

By late June, the Trump administration released the first federal data sets accounting for this change. The figures do not merely reflect those who signed up; they account for "realized" coverage—individuals who completed the enrollment process, survived the verification period, and paid their first monthly premiums. Cynthia Cox, director of the ACA program at the healthcare research nonprofit KFF, noted that the data also accounts for those retroactively removed from coverage following the conclusion of grace periods for nonpayment. The result is a grim picture of a system in retreat.

A Closer Look at the Data: Where the Losses Hit Hardest

The impact of the subsidy expiration has not been distributed evenly across the United States. According to an Associated Press analysis of the new federal data, Ohio and Oklahoma bore the brunt of the volatility, each experiencing a staggering decline of more than 32% in ACA enrollment.

The "tier-one" of states hit by the decline—those losing more than a quarter of their enrollees—includes a geographically diverse group: Arizona, South Carolina, Minnesota, Indiana, Michigan, Mississippi, Louisiana, and Missouri.

Florida, which has long served as a bellwether for the ACA due to its high concentration of gig workers, entrepreneurs, and its historical refusal to expand Medicaid, presents the most complex case. Despite remaining the state with the highest total enrollment at approximately 4 million, it also recorded the largest raw loss in coverage, with roughly 443,000 residents dropping off the rolls.

The New Mexico Exception

Amidst this nationwide contraction, New Mexico stands alone. It is the only state in the country to report an increase in its covered population, showing a 14% growth compared to the previous year. This statistical anomaly is directly linked to proactive state policy. Recognizing the fiscal cliff created by the expiration of federal subsidies, the New Mexico legislature held a special session to secure state-level funding to bridge the gap. In March 2026, the governor signed legislation extending this local subsidy program through mid-2027, effectively insulating its residents from the federal cost-shock.

The Divergence Between State and Federal Marketplaces

A critical takeaway from the data is the disparity between states that utilize the federal marketplace (Healthcare.gov) and those that operate their own state-based exchanges.

Approximately three in five states rely on the federal portal. The data suggests that these states saw significantly larger shares of enrollment losses compared to their counterparts with state-run exchanges. Analysts point to a simple reason: many states with their own marketplaces moved swiftly to leverage local budget surpluses or state-specific taxes to offset the loss of federal dollars. By creating "state-only" subsidy buffers, these jurisdictions were able to prevent the catastrophic premium spikes that drove citizens off the federal platform.

Official Responses and Competing Narratives

The Department of Health and Human Services (HHS) has offered a nuanced, if somewhat controversial, explanation for the figures. In a report published last week, HHS officials suggested that a portion of the enrollment decline could be attributed to a concerted federal crackdown on fraudulent or "phantom" enrollments—a problem that has plagued the system for years as bad actors exploited loopholes to siphon commissions.

However, independent health analysts remain skeptical that fraud prevention accounts for the scale of the 2.6 million drop. "This is in line with our expectations regarding cost sensitivity," said KFF’s Cynthia Cox. "While there may be some cleanup of fraudulent accounts, the primary driver is clearly the expiration of financial assistance. When people see their monthly premiums double, the math simply stops working for the average household."

Furthermore, administrative hurdles—such as tightened requirements for immigrant access to subsidized plans—have also contributed to the thinning of the marketplace. These changes have created a "perfect storm" for potential enrollees, who are now facing higher costs, more complex eligibility requirements, and less financial support.

Implications: Healthcare as an Election-Year Issue

As the nation moves toward the November elections, healthcare affordability has surged to the forefront of the voter agenda. For millions of Americans, the ACA has transitioned from a stable safety net to a source of monthly financial anxiety.

The "Place of Last Resort"

The most pressing question raised by the decline is: where are these 2.6 million people going?

The data does not explicitly track the post-marketplace trajectory of former enrollees. It is possible that some have transitioned to employer-sponsored insurance or other private plans. However, health experts express deep concern that a vast majority of those who left the marketplace are now uninsured.

"The ACA marketplace is, for many, a place of last resort," Cox explained. "If you aren’t eligible for Medicaid and you don’t have an employer plan, you don’t have many other places to go. When people drop out of the marketplace, they aren’t necessarily ‘graduating’ to better insurance—they are often opting out of coverage entirely because they simply cannot afford the bill."

The Economic and Political Ripple Effect

The political fallout is already evident. With affordability being a top-tier concern for voters across the political spectrum, the decline in enrollment is providing fresh ammunition for debate.

- For the proponents of the ACA: The decline serves as a cautionary tale about the fragility of federal subsidies. They argue that the reliance on temporary, "enhanced" measures created a cliff that was always destined to be dangerous if not made permanent.

- For the skeptics: The decline is presented as evidence that the ACA is inherently unstable and reliant on unsustainable federal spending that masks the true cost of healthcare.

The economic implications are equally concerning. As enrollment drops, the risk pool in the insurance marketplace may narrow, potentially leading to adverse selection where only those with the most significant health needs remain, thereby driving up premiums further for those who stay. This cycle of rising costs and declining participation could jeopardize the viability of the marketplaces in the coming years.

Conclusion: A System at a Crossroads

The 2026 enrollment data serves as a stark reminder of how policy decisions at the federal level resonate through the lives of millions. As households struggle to absorb the loss of subsidies, the American healthcare system faces a critical juncture.

Will states follow the model of New Mexico and take the lead in stabilizing their own marketplaces? Will Congress reconsider the political cost of the subsidy expiration? Or is the nation entering a new era where millions are priced out of the private insurance market, returning to a state of widespread under-insurance?

For now, the data confirms a sobering reality: the promise of affordable, accessible healthcare remains a tenuous work in progress, subject to the whims of legislative cycles and the unforgiving math of the marketplace. As voters head to the polls this November, the 2.6 million citizens who lost their coverage will be a silent but powerful force in the conversation, representing a growing segment of the population that feels left behind by the current direction of national health policy.