The global financial markets are currently gripped by an unprecedented fervor surrounding Artificial Intelligence. Trillions of dollars in capital are being funneled into AI research, data center infrastructure, and semiconductor manufacturing, all under the premise that we are witnessing the next industrial revolution. However, a growing cohort of industry veterans, financial analysts, and systemic risk experts argue that the current AI landscape is not built on a foundation of genuine productivity, but rather on a speculative mania fueled by cheap debt, circular capital flows, and untenable financial projections.

As the industry pivots toward massive, multi-year loss cycles, the question is no longer whether the bubble will burst, but how much collateral damage the wider economy will sustain when the music stops.

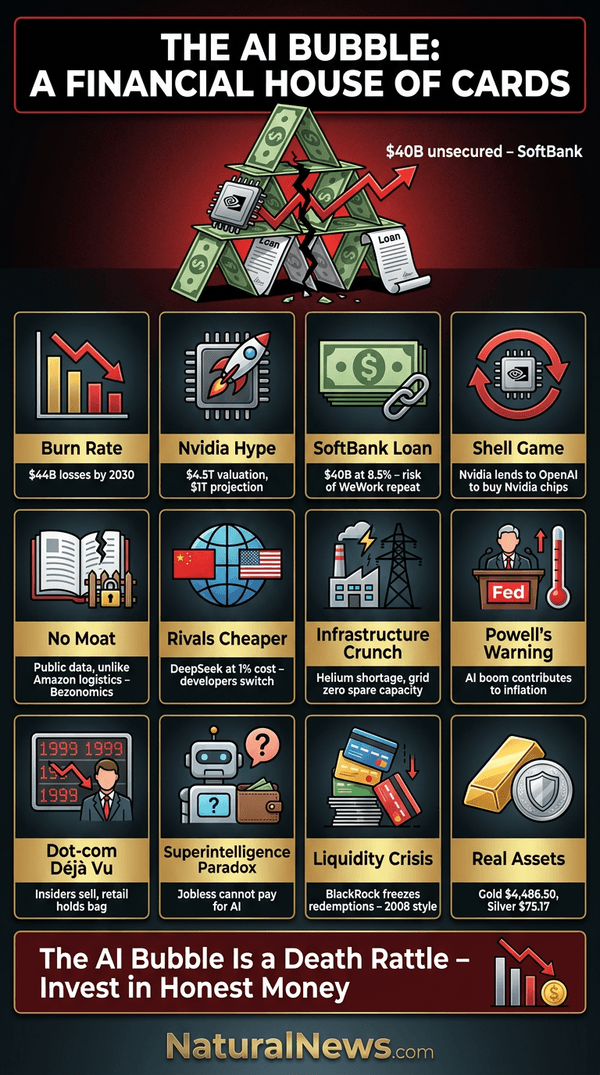

The Anatomy of the Bubble: Main Facts and Financial Reality

At the epicenter of this controversy lies OpenAI, a firm that has become the poster child for the "growth-at-any-cost" mentality. Despite its massive market presence, OpenAI’s financials paint a picture of a "savage black hole" for capital. Projections suggest the company could hemorrhage upwards of $44 billion over the next five years, with no clear path to profitability until at least 2030.

Analysis from institutions like HSBC highlights a staggering liquidity requirement: OpenAI may need an additional $207 billion by 2030 merely to maintain its operational solvency. This demand is driven primarily by astronomical cloud compute costs, which are forecasted to hit $792 billion annually by the end of the decade.

This capital expenditure model is increasingly circular. Critics point to the relationship between Nvidia and its primary customers, such as OpenAI. In a feedback loop of risk, major chip manufacturers are effectively facilitating the funding of their own customers. OpenAI secures loans—often unsecured and at high interest rates—to purchase hardware from vendors who then report record-breaking earnings, which in turn fuels further investment into the AI startups. This "synthetic demand" creates a house of cards that benefits early insiders and institutional players while leaving the broader market vulnerable to a sudden correction.

A Chronology of Reckless Capital Allocation

To understand how the market reached this inflection point, one must look at the recent timeline of institutional bets:

- The SoftBank Infusion: SoftBank recently extended a $40 billion unsecured loan to OpenAI. With an 8.5% interest rate and a short 12-month maturity, the loan structure mirrors the high-risk, high-leverage gambits that defined the collapse of WeWork.

- Revenue Misses and Internal Alarm: Recent reports indicate that OpenAI is trailing behind its aggressive revenue and user-growth targets. Internal memos from the company’s CFO have reportedly expressed concern that current commitments exceeding $1.5 trillion may be impossible to fulfill, signaling a massive disconnect between valuation and reality.

- The Rise of Global Competition: The "first-mover advantage" once claimed by U.S.-based frontier models has been significantly eroded. Developers are increasingly migrating toward alternatives like Anthropic, DeepSeek, and Qwen. Notably, Chinese-developed models are now delivering superior engineering and mathematical performance at roughly 1% of the cost of their American counterparts, fundamentally undermining the pricing power of the current market leaders.

Supporting Data: Why the "Amazon Moat" is a Mirage

Bulls frequently compare the AI boom to the rise of Amazon, arguing that massive upfront capital investment will create an unassailable "moat." However, this analogy fails under scrutiny. Amazon’s success was predicated on a tangible, proprietary logistics network—warehouses, delivery fleets, and supply chain infrastructure that were nearly impossible to replicate.

In contrast, OpenAI and similar AI labs rely on the same public internet corpus for model training. There is no physical barrier to entry, no proprietary data advantage, and no unique operational infrastructure that cannot be mimicked by competitors with sufficient compute. Because every lab can access the same datasets, the value proposition of the models is rapidly commoditizing. When a competitor offers 95% of the performance at 1% of the cost, the "moat" disappears, and the business model shifts from a high-margin enterprise to a low-margin utility.

The Physical Constraint: A Physics Problem, Not a Finance Problem

Even if capital were infinite, the physical limitations of the real world provide a hard ceiling for AI growth. The buildout of AI infrastructure is being throttled by a series of supply chain and resource crises:

- The Helium and Semiconductor Crunch: Advanced chip manufacturing requires helium, a gas primarily sourced from the Persian Gulf. Geopolitical instability in that region has crippled the supply chain, making it physically impossible to fabricate the next generation of GPUs at the scale demanded by current forecasts.

- The Energy Grid Deficit: Federal Reserve Chair Jerome Powell and other economic observers have noted that the massive energy demands of new data centers are contributing to inflationary pressures. In parts of the eastern United States, the power grid has zero spare capacity to accommodate the massive, 24/7 power draws required by these facilities.

- Construction Timelines: You cannot "will" factories and power plants into existence through venture capital fundraising. The time required to procure gas turbines, copper wiring, and specialized construction equipment creates a lag that the current market valuation—which assumes exponential, uninterrupted scaling—fails to account for.

Official Responses and Economic Implications

The Federal Reserve and major financial institutions have begun to signal unease. Private credit markets, which were once the engine of the AI boom, are showing signs of locking up. BlackRock and other major firms have reportedly moved to freeze redemptions, a classic indicator of a liquidity crunch.

Economist Ed Dowd has warned that the "real" economy—the sector comprised of manufacturing, logistics, and consumer goods—is failing to keep pace with the hyper-inflated valuations of AI tech stocks. If the AI bubble bursts, the contagion will likely spread to the banking sector, where unsecured loans to AI startups will be marked down to zero, leading to a 2008-style cascade.

The irony is that the technocrats pushing this agenda may be setting the stage for their own obsolescence. If "superintelligence" were to actually arrive, its primary economic impact would be the displacement of millions of workers. A jobless population lacks the disposable income to purchase the products or services offered by these AI companies, creating a terminal paradox for their revenue models.

Conclusion: Preparing for the Correction

History has shown that every speculative bubble insists, "this time is different." From the Dutch Tulip Mania to the Dot-com crash of 2000, the narrative remains the same: capital floods in, valuations soar on promises of a future that has yet to arrive, and insiders cash out before the inevitable reality check.

For the prudent investor, the signs are clear. The AI sector, as currently structured, resembles a death rattle for a financial system built on debt and deception. As the liquidity cycle turns and interest rates remain stubbornly high, the "AI Miracle" will likely be revealed as a temporary mirage.

When the dust finally settles, the infrastructure will remain—empty data centers and idle GPUs waiting to be repurposed for meaningful, sustainable human progress. Until then, those who prioritize capital preservation—focusing on tangible assets like gold, silver, and essential resources—will be the ones in a position to rebuild the economy on a more rational, productive, and stable foundation. The AI bubble is not a path to a new golden age; it is a warning of the fragility of a market that has abandoned the basic principles of profit, cost-efficiency, and physical reality.